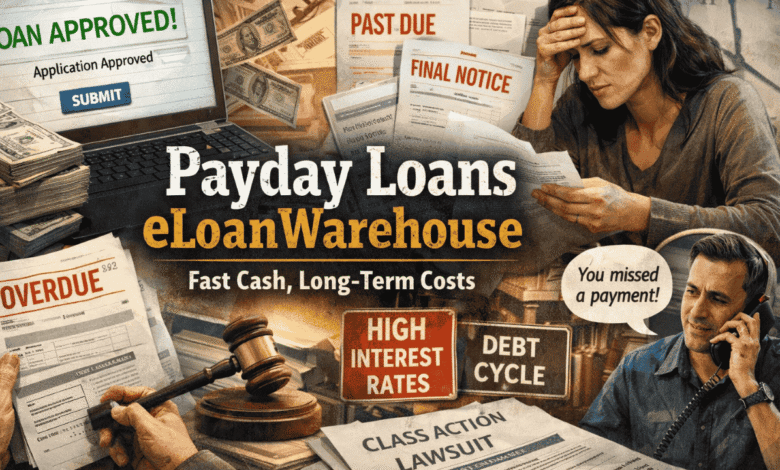

payday loans eloanwarehouse: what borrowers actually experience when fast cash turns complicated

Anyone searching for fast money already knows the stakes are high. Rent is due, a car won’t start, or a medical bill landed at the worst moment. That’s where payday loans eloanwarehouse usually enter the picture. Not as a curiosity, not as a trend, but as a last-resort decision made under pressure. The problem isn’t that these loans exist. The problem is what happens after the money hits your account.

This isn’t a sales pitch or a warning label written in fine print language. It’s a straight look at how payday loans eloanwarehouse operate in the real world, how borrowers describe the experience, and where the risks actually sit.

How payday loans eloanwarehouse position themselves to desperate borrowers

Payday loans eloanwarehouse don’t present themselves as old-school payday lenders standing behind bulletproof glass. The branding is cleaner. The language leans toward installment loans, flexibility, and breathing room. Longer repayment periods are front and center, especially compared to single-paycheck loans that demand full repayment in weeks.

The pitch works because it hits a nerve. Instead of asking for everything back on your next paycheck, the structure spreads payments out across months. For borrowers already drowning, that sounds reasonable. In practice, the timeline doesn’t erase the core issue. High-cost borrowing remains high-cost borrowing, just stretched over time.

Applicants are drawn in by speed. Online forms, minimal credit barriers, and fast funding dominate the experience. When banks shut the door and credit cards are maxed out, payday loans eloanwarehouse look like a lifeline rather than a trap.

Approval is easy; the real test comes later

The application process for payday loans eloanwarehouse is rarely the issue. Borrowers consistently report that getting approved feels simple, sometimes deceptively so. Income verification, a checking account, and a phone call or two can be enough to move things forward.

That ease is intentional. When approval feels frictionless, urgency wins. Few people slow down to calculate what months of payments at high interest actually look like. By the time the math becomes clear, the loan is already active.

What’s striking is how often borrowers say the terms felt different once repayment began. Scheduled withdrawals, compounding interest, and fees become more visible after the initial relief fades. The problem isn’t confusion; it’s timing. Clarity arrives too late.

Installment structure doesn’t automatically mean safer debt

One of the biggest selling points of payday loans eloanwarehouse is the installment model. Compared to traditional payday loans, it sounds like progress. And in narrow cases, it is. Paying over time can prevent the single massive hit that wipes out an entire paycheck.

But installment debt with steep interest doesn’t stop being expensive just because it’s broken into pieces. Borrowers often underestimate how much they’ll repay in total. Monthly payments feel manageable until stacked against rent, utilities, groceries, and unexpected expenses.

This is where payday loans eloanwarehouse quietly resemble the very payday cycle they claim to soften. Miss a payment, fall behind, or need another loan before finishing the first, and the debt snowballs. The structure delays the pain; it doesn’t eliminate it.

Interest rates and costs: the part borrowers regret not calculating

Ask borrowers what they wish they had looked at more closely, and interest comes up fast. Payday loans eloanwarehouse are frequently described as expensive, even by people who expected high costs going in.

The issue isn’t just the rate itself. It’s the total repayment amount over time. When loans run for months, the cumulative cost becomes easier to ignore at the start and harder to stomach later.

Several borrowers describe feeling locked in. Paying off early isn’t always realistic when budgets are already stretched thin. Each payment reduces the balance slowly, which feeds frustration and fatigue. The debt lingers longer than expected.

Customer complaints focus less on money and more on pressure

Money is only part of the story. Reviews and complaints around payday loans eloanwarehouse repeatedly point to customer service and collections as stress multipliers. Borrowers talk about persistent calls, rigid policies, and a tone that shifts once payments are due.

This shift catches people off guard. The friendly approval stage contrasts sharply with repayment enforcement. For borrowers already under financial strain, the emotional toll matters as much as the dollars.

Not every borrower has a negative experience. But patterns matter. When similar complaints surface across different platforms, it signals a system optimized for collection, not flexibility.

Legal scrutiny adds another layer of risk borrowers don’t consider

Most borrowers don’t think about legal structures when applying for payday loans eloanwarehouse. They’re thinking about groceries or a repair bill. That’s understandable. Still, legal disputes around lending practices raise real concerns.

Allegations tied to lending models designed to bypass state interest caps have surfaced in public records. Whether or not individual cases succeed, the presence of legal scrutiny alone matters. It highlights how aggressive lending strategies can push against regulatory boundaries.

For borrowers, this doesn’t translate into immediate relief. It translates into uncertainty. Loans tied up in legal gray areas don’t become easier to repay. They just add another layer of complexity.

Who payday loans eloanwarehouse actually work for

There’s a narrow group of borrowers for whom payday loans eloanwarehouse can serve a temporary purpose. People with stable income, a clear payoff plan, and no intention of repeat borrowing can sometimes use them as a short bridge.

The key word is temporary. These loans are least damaging when treated like an emergency tool, not a financial strategy. The moment they become routine, the math turns hostile.

Anyone already juggling multiple debts, unstable income, or unpredictable expenses is taking on serious risk. For those borrowers, payday loans eloanwarehouse often worsen the problem they’re meant to solve.

Better questions borrowers should ask before applying

Most regret comes from unasked questions. Before committing to payday loans eloanwarehouse, borrowers should pressure-test the decision.

How much will this loan cost me if I make every payment on time? What happens if I miss one? Can I realistically pay this off without borrowing again? If the answer to any of these is unclear, that’s a warning, not a detail to ignore.

Alternatives exist, even if they take more effort. Credit unions, payment plans with creditors, and income-based assistance programs don’t offer instant cash, but they also don’t trap borrowers in long-term high-cost debt.

Why payday loans eloanwarehouse keep attracting borrowers anyway

Despite the risks, payday loans eloanwarehouse continue to attract users for one reason: they show up when others don’t. Traditional lenders reject quickly and impersonally. These loans respond fast and say yes.

Speed has value, especially in emergencies. But speed also bypasses reflection. When survival mode kicks in, future costs feel abstract. That’s the environment where these loans thrive.

Understanding that dynamic doesn’t require moral judgment. It requires honesty. Payday loans eloanwarehouse succeed because they meet immediate needs, not because they offer healthy outcomes.

The uncomfortable truth borrowers learn too late

The hardest lesson many borrowers share is simple: relief is temporary, repayment is not. Payday loans eloanwarehouse provide short-term breathing room at the cost of long-term pressure.

That doesn’t make borrowers irresponsible. It makes the system predictable. High-cost lending flourishes where financial buffers are thin and emergencies are common.

The real question isn’t whether these loans should exist. It’s whether borrowers are given enough clarity, time, and alternatives to avoid repeating the cycle. Right now, too many learn the answers after signing.

Conclusion

Payday loans eloanwarehouse don’t fail because borrowers misunderstand them. They fail because urgency beats calculation, and relief arrives before reality. Used once, carefully, with a clear exit, they can serve a narrow purpose. Used casually or repeatedly, they deepen financial strain.

If you’re considering this path, pause longer than the application asks you to. The speed that feels like a gift today can become the weight you’re carrying months from now.

FAQs

- Can payday loans eloanwarehouse be paid off early without penalties?

Early payoff policies vary by loan agreement. Borrowers should confirm whether paying early reduces total interest or simply accelerates scheduled payments. - Why do payments sometimes feel harder than expected with payday loans eloanwarehouse?

Monthly amounts may look manageable in isolation, but combined with existing bills and expenses, they often strain already tight budgets. - Do payday loans eloanwarehouse affect credit scores?

The impact depends on reporting practices and payment behavior. Missed payments are more likely to cause damage than on-time ones to create improvement. - What happens if income changes during repayment?

Many borrowers report limited flexibility once a loan is active. Income loss can quickly turn manageable payments into missed ones. - Are repeat loans common with payday loans eloanwarehouse?

Yes. Borrowers who rely on these loans more than once often struggle to fully exit the repayment cycle without external help.